- Your cart is empty

- Continue Shopping

Product Description

Every dollar you send to debt is a dollar that will never build your wealth.

The average household pays over $1,000 per month in debt minimum payments. That is $12,000 per year — the equivalent of a significant salary raise — flowing to lenders in exchange for nothing. It funds no asset. It builds no equity. It creates no future. It simply services the past. The Debt-Free Blueprint is the complete system for ending that cycle.

Debt is not purely a maths problem. If it were, everyone who understood compound interest would already be debt-free. The research is clear: debt is primarily a behavioural and psychological problem — driven by present bias, emotional spending, social comparison, and the minimum payment trap that keeps balances alive for decades. This guide addresses all of it: the numbers, the strategy, and the psychology.

More importantly, it addresses what comes after. The discipline you build eliminating debt is the same discipline that builds wealth. The Debt-Free Blueprint ends with a complete transition plan for the month your last payment clears — so the cash flow that was going to creditors starts compounding for you instead.

What’s Inside — 8 Chapters + 5 Worksheets

Introduction — The True Cost of Debt

How debt silently dismantles financial futures. The real number: not the interest rate but the compounding wealth you will never build. What this guide will give you.

Chapter 1 — Understanding Your Debt — The Complete Picture

The debt inventory process. How compound interest works against you. The minimum payment trap. Calculating your debt-free date. Good debt vs bad debt — the framework for prioritisation.

Chapter 2 — The Debt Payoff Methods — Snowball vs Avalanche

Both methods explained in full. The psychological case for snowball. The mathematical case for avalanche. The hybrid approach. Debt consolidation — when it helps and when it is a trap.

Chapter 3 — Building Your Debt-Free Budget

Why most budgets fail. The zero-based budget framework for debt elimination. Automating your payoff. Spending tracking — the first 90 days. Category-by-category budget building.

Chapter 4 — Accelerating Your Payoff

Finding extra money without significant lifestyle sacrifice. Subscription audit. Food and grocery optimisation. Bill negotiation scripts. Salary negotiation. Side income specifically earmarked for debt. The windfall rule.

Chapter 5 — Dealing with Specific Debt Types

Credit cards — balance transfer strategy and stopping the bleeding. Student loans — rate-based approach framework. Car loans — avoiding the negative equity trap. Medical debt — negotiation and hardship programmes.

Chapter 6 — The Psychology of Debt

Present bias. Social comparison and lifestyle inflation. Emotional spending triggers. The fresh start effect. Building psychological resilience for a multi-year payoff journey.

Chapter 7 — Staying Debt-Free

The relapse prevention plan. The four pillars: emergency fund, permanent budget, the debt decision rule, and a wealth-building destination. Credit score after debt.

Chapter 8 — Life After Debt — Building Wealth from Zero

The transformation: the money that was going to creditors is now yours. The immediate post-debt checklist. The compounding future — what consistent investment from debt-free looks like over 25 years.

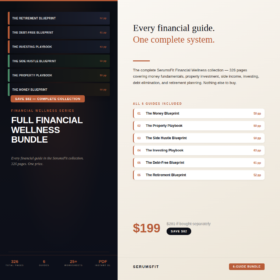

Appendices include: Complete debt inventory worksheet, zero-based budget template, subscription audit and bill negotiation tracker, monthly debt payoff progress tracker (12 months), and life after debt transition plan with worksheets.

Who This Is For

- You carry credit card, personal loan, student loan, or car finance debt and want a clear plan

- You have tried to pay off debt before and run out of motivation before finishing

- You pay minimums every month and know the balance is barely moving

- You do not know exactly how much you owe or what the total interest is costing you

- You want to understand why you keep accumulating debt even when you intend not to

- You are ready to make the transition from servicing the past to building the future

What Makes This Different

- Both methods in full. Snowball and avalanche are both explained in detail, with clear guidance on which to choose and when a hybrid approach makes most sense.

- Psychology treated as seriously as strategy. Most debt guides give you a spreadsheet. This one explains why you are in debt and what to do about the behaviour, not just the balance.

- Worksheets throughout. The debt inventory, budget template, negotiation tracker, and progress tracker are ready to complete — not exercises to design yourself.

- Ends with wealth building. The guide does not stop at zero. It gives you the exact transition plan so debt freedom becomes the starting line, not the finish line.

- Realistic, not extreme. The payoff plan is designed to be sustainable — not a deprivation system that leads to backlash spending.

30-Day Money-Back Guarantee

Complete your debt inventory. Choose your payoff method. Make your first extra payment above the minimum. If you have done these three things within 30 days and do not feel significantly more in control of your finances, email us for a full refund.

Product Details

- Format: Instant download PDF

- Pages: 61 (A4, professionally designed, print-ready)

- Language: English

- Compatible with: Any PDF reader, tablet, phone, or printer

- Delivery: Instant — download link on confirmation page and by email

- Published by: SerumsFit | serums.fit | 2026

This guide is for educational purposes only and does not constitute financial or debt advice. If you are experiencing serious financial difficulty, please contact a qualified debt adviser or non-profit credit counselling organisation.

© 2026 SerumsFit. All rights reserved. For personal use only.

5 reviews for The Debt-Free Blueprint — The Complete System for Eliminating Debt and Building Real Wealth

Only logged in customers who have purchased this product may leave a review.

Rachel P. –

Most debt advice online is either basic (stop buying coffee) or extreme (sell your car and live on rice). This guide is neither. It takes you through a structured system that accounts for real life — the budget framework is realistic, the psychology chapter is genuinely insightful, and the transition plan for after you become debt-free is something I have not seen anywhere else. I cleared four debts in eleven months.

Marie-Claire F. –

I appreciated that this guide doesn’t make you feel stupid or irresponsible for having debt. It treats debt as a practical problem with a practical solution and gets on with solving it. The minimum payment trap section was genuinely shocking — I had no idea how long it would take to pay off my credit card at minimum payments.

George L. –

I knew what to do about my debt intellectually — pay more than the minimum, prioritise high interest, do not borrow more. Knowing and doing are different things. This guide addresses that gap. The section on present bias and why smart people make poor financial decisions in the moment was the piece I was missing. Understanding my own decision-making patterns changed the behaviour.

Samantha R. –

I had $22,000 of credit card and personal loan debt when I bought this guide. Fourteen months later I’m debt-free. I used the avalanche method, followed the zero-based budget framework religiously, and found an extra $400 per month by going through the expense reduction section properly. The psychology chapter was important too — understanding present bias helped me stop making impulsive purchases.

Ian C. –

I’ve had low-level financial anxiety for years because I had debt but no plan for dealing with it. This guide gave me a plan. Just having a clear system reduced my anxiety significantly before the balance had even dropped much. I’m 8 months in, two debts cleared, one remaining. The snowball method was right for me — each payoff genuinely motivated me to keep going.